Are You Aware? A VA or FHA Loan Assumption Could Be Your Smartest Move in Santa Clara County

In today’s real estate market, finding affordable home financing options can be challenging. With rising rates and tighter budgets, homebuyers across Santa Clara County are searching for smarter ways to buy homes. One often-overlooked opportunity is a loan assumption. This option allows buyers to take over a seller’s existing mortgage, potentially saving thousands in interest and fees. Whether you are considering a VA loan assumption or an FHA loan assumption, understanding how these programs work can help you make an informed and cost-effective decision.

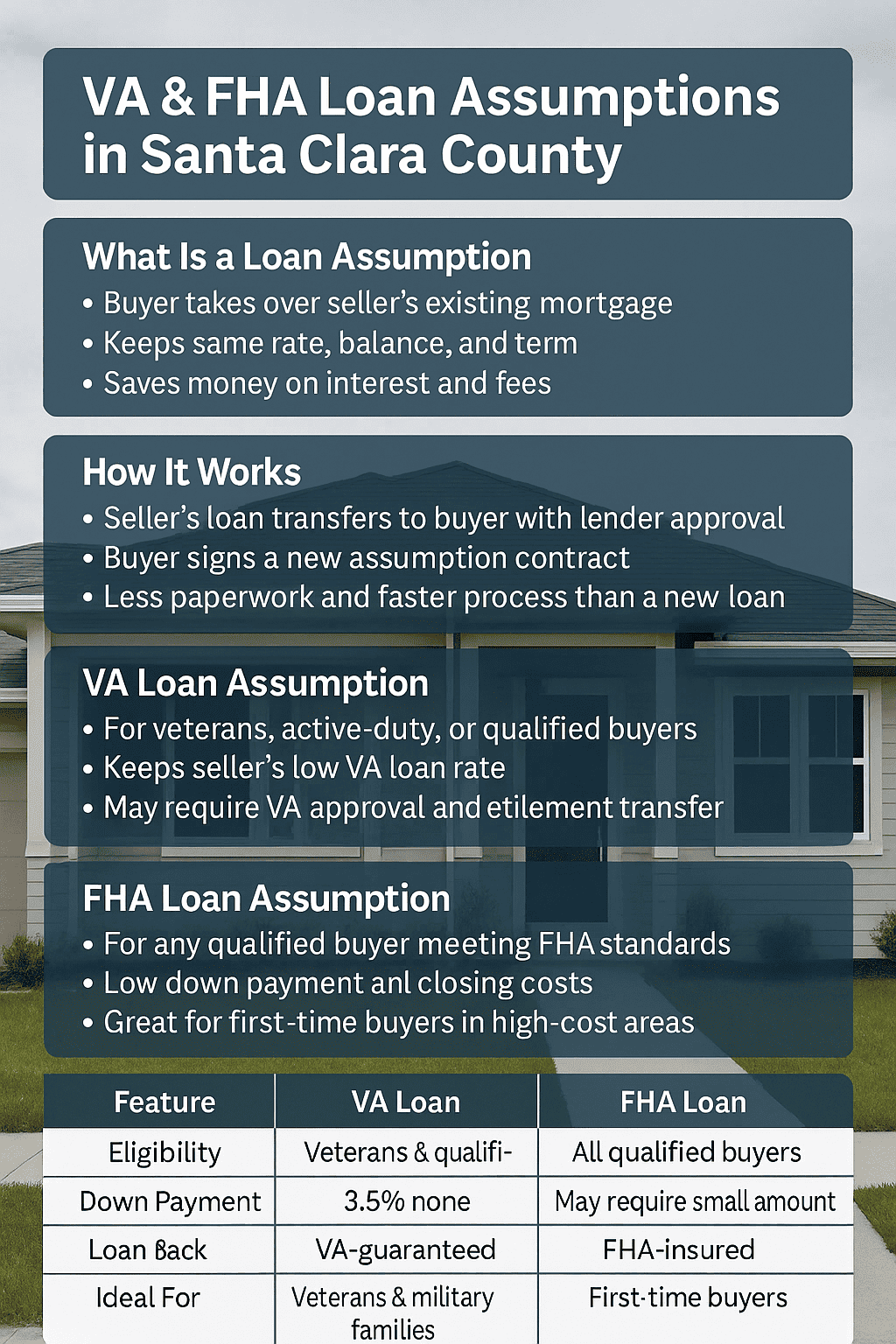

What Is Loan Assumption

Before exploring the benefits, it’s important to understand what is loan assumption. Simply put, it means a buyer takes over the seller’s existing mortgage instead of getting a new one. The buyer agrees to continue making payments based on the same interest rate, loan balance, and remaining term of the original mortgage.

This approach can be highly beneficial in a market like Santa Clara County, where mortgage rates are often higher than in previous years. By assuming a loan that carries a lower rate, buyers can enjoy significant long-term savings.

How a Mortgage Loan Assumption Works

A mortgage loan assumption works by transferring the seller’s current mortgage and its terms to the new buyer. Both parties must agree, and the lender must approve the transfer. Once approved, the buyer becomes responsible for making monthly payments.

The process typically involves verifying credit, reviewing income, and signing a new loan assumption contract. This document outlines the terms of the transfer, including any fees or remaining balance to be covered at closing.

For buyers, this means less paperwork compared to applying for a new mortgage, and for sellers, it can make their home more attractive to potential buyers.

VA Loan Assumption Explained

A VA loan assumption is available to eligible military service members, veterans, or qualified buyers who take over an existing VA-backed mortgage. The biggest advantage is the ability to keep the low interest rate of the original loan.

In Santa Clara County, where property prices are high, assuming a VA loan can lead to significant savings over time. However, the buyer must meet the VA’s qualification standards, and the seller’s VA entitlement could remain tied to the loan unless it is officially transferred.

This makes it important to work closely with lenders and the Department of Veterans Affairs to ensure all requirements are met before closing.

FHA Loan Assumption Explained

An FHA loan assumption is similar but designed for loans insured by the Federal Housing Administration. Buyers who assume an FHA loan also benefit from lower rates and reduced closing costs.

The qualification process is straightforward since FHA loans are meant to help a wider range of borrowers. The buyer must demonstrate the ability to make payments and agree to the loan’s existing terms.

In Santa Clara County, this option can be ideal for first-time buyers who want predictable payments and lower upfront expenses while purchasing a home that already carries an FHA mortgage.

VA vs. FHA Loan Assumption: Key Differences

Here’s a simple comparison table showing how these two popular loan assumption programs differ:

This comparison helps you identify which program suits your needs best in Santa Clara County.

Benefits of a Home Loan Assumption

A home loan assumption can be an excellent financial move in a rising-rate environment. Here are some of the main benefits:

- Lower interest rates – Buyers can keep the seller’s existing rate, which is often lower than current market rates.

- Reduced closing costs – Loan assumptions generally have fewer fees than new mortgages.

- Simplified process – Less documentation and faster approval compared to new loan applications.

- Increased home value appeal – Sellers can attract more buyers if their existing loan terms are favorable.

For Santa Clara County homeowners and buyers, these benefits can make a big difference in affordability.

Understanding the Loan Assumption Contract

The loan assumption contract is a legal agreement that finalizes the transfer between the seller and the buyer. It defines the responsibilities of both parties, confirms the remaining loan balance, and specifies any costs involved in the process.

It is crucial that both the buyer and seller review this contract carefully, ideally with the help of a mortgage professional or attorney. This ensures that all terms are clear and that the buyer is protected against any prior obligations from the seller.

Why Loan Assumption Makes Sense in Santa Clara County

Santa Clara County’s housing market remains one of the most competitive in California. Rising home values and higher mortgage rates have made affordability a major challenge.

A loan assumption gives buyers an advantage by allowing them to secure a lower rate on a property that might otherwise be out of reach. Sellers also benefit by marketing their homes with an assumable loan, making them more attractive to potential buyers who want to save on financing.

This strategy aligns perfectly with current market conditions, where preserving favorable loan terms can provide real financial relief for both sides.

Final Thoughts

A loan assumption can be a smart, cost-saving move for homebuyers in Santa Clara County. Whether through a VA home loan assumption or an FHA loan assumption, taking over an existing mortgage allows you to enjoy better terms and smoother approval.

Before proceeding, always discuss your options with experienced lenders familiar with mortgage loan assumption programs. They can help guide you through the process, review your eligibility, and ensure that the loan assumption contract is handled correctly from start to finish.

Frequently Asked Questions

1. What is loan assumption and how does it work?

Loan assumption allows a buyer to take over a seller’s existing mortgage, keeping the same interest rate and repayment terms with lender approval.

2. Who can qualify for a VA loan assumption?

VA loan assumptions are available to eligible veterans, active-duty members, or qualified buyers who meet VA credit and income requirements.

3. Is an FHA loan assumption easier to get than a new loan?

Yes, an FHA loan assumption often has simpler qualification requirements and lower costs compared to applying for a new mortgage.

4. Why is loan assumption popular in Santa Clara County?

Loan assumptions help buyers save money by keeping older, lower-rate mortgages — a big advantage in areas like Santa Clara County where rates and prices are high.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)